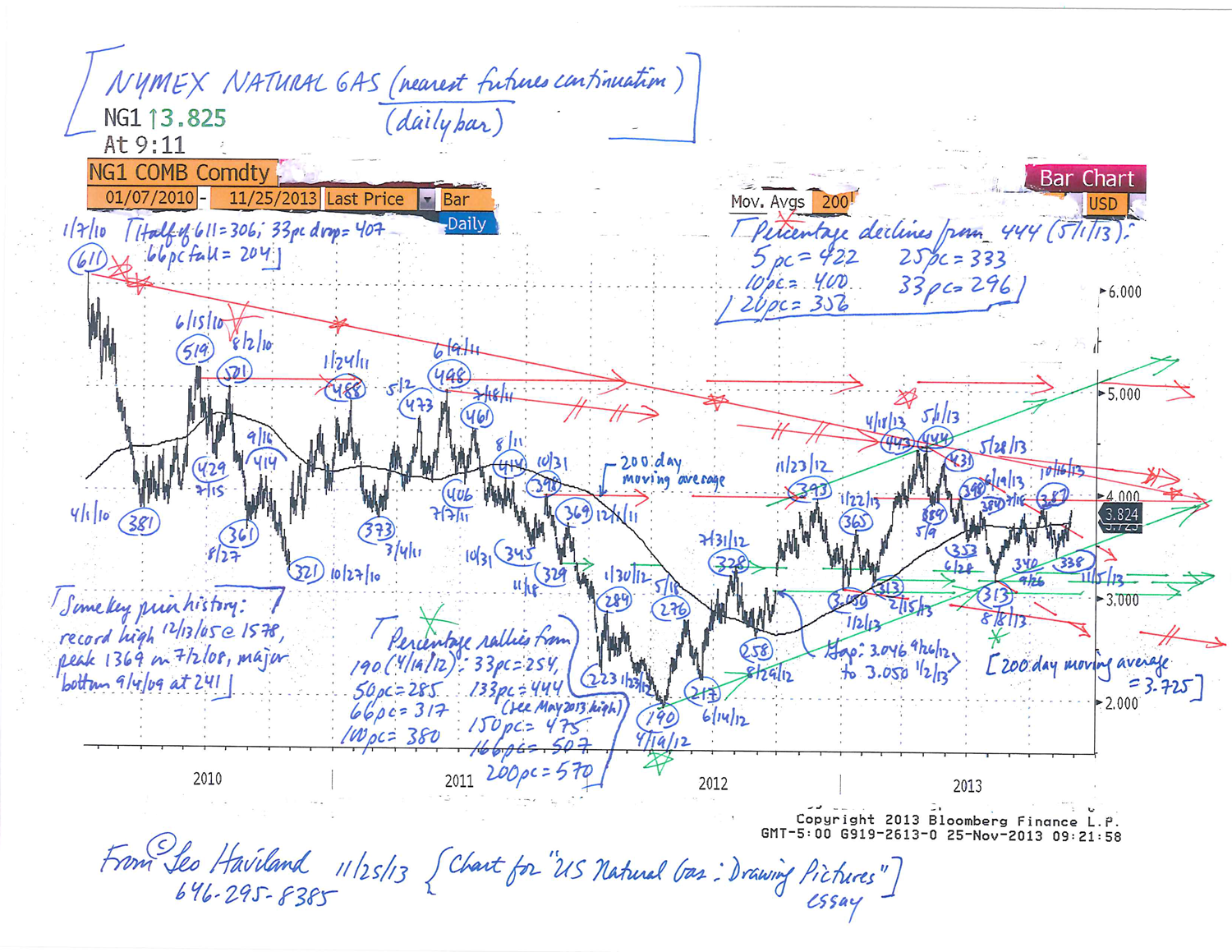

ROLLIN’ AND TUMBLIN’ IN US NATURAL GAS © Leo Haviland April 20, 2015

In all marketplace battlefields, a wide variety of storytellers select between (and emphasize differently) an array of variables. They thereby generate diverse bullish and bearish arguments that heatedly compete for allegiance and action. And analysis and trading always are difficult enterprises. However, in the United States natural gas universe nowadays, the noise, smoke, and uncertainty produced by these diverse variables and conflicting perspectives and recommendations make it especially challenging to boldly swear unquestioning loyalty to a particular marketplace viewpoint.

What does historical analysis of major United States natural gas bear marketplace moves (NYMEX nearest futures continuation basis) in the context of days coverage reveal regarding the ending of the major bear trend that emerged in late February 2014? Perhaps 4/13/15’s 2.475 low was an important trough; however, several days of course remain in April and many key bottoms have occurred around contract expiration. If a noteworthy bottom is not established in calendar April 2015, the most probable time for a major low is in late August/calendar September 2015. NYMEX natural gas reached many important bottoms in late calendar August and September. However, a final low in late summer 2015 would stretch out the February 2014 bear marketplace trend substantially longer than the historical average.

In any case, if NYMEX natural gas prices pierce 4/13/15’s low (nearest futures continuation), that level probably will not be broken by much. Substantial support lurks around 2.40 and 2.20/2.15.

****

End March 2015’s 20.0 days of coverage (1471bcf divided by about 73.5bcf/day of full calendar year 2014 consumption), though way up from March 2014’s 12.0 days coverage, dips slightly under the 21.8 days end March 1990-2014 average. It also falls a notable, though not extreme, 4.1 days beneath the nine year 2006-14 average. Thus despite the notable arithmetic stock increase during calendar 2014 build season, the national days coverage inventory picture at the end of winter 2014-15 draw season is slightly bullish.

What’s the bottom line in regard to the natural gas bear trend that began in February 2014 if one concentrates on the natural gas inventory variable? With the NYMEX nearest futures natural gas price currently well under 4.00, this end winter 2014-15 inventory factor “taken by itself”, looks neutral to supportive for gas prices. This fundamental consideration should be interpreted alongside the marketplace history relating to price and time factors.

End October 2015’s 49.5 days coverage level slides 6.3 days beneath the 2006-14 end October average of 55.8 days and 4.1 days under 1990-2014’s 53.6 days. This end October 2015 days coverage total therefore is bullish (even if not wildly so given prospects of increased natural gas production).

Look further out in the murky future to March and October 2016. Although much of course can happen between now and then, potential days coverage nevertheless does not suggest notable oversupply relative to historic averages.

The EIA forecasts end March 2016 inventory at 1704bcf and end October 2016 stocks at 3923bcf. Days cover at end March 2016 will be around 22.3 days (1704bcf/76.3bcf/d). Though this is slightly (.5 day) above the 21.8 day 1990-2014 average, it is 1.8 day less than 2006-14’s 24.1 day average. October 2016’s hypothetical days coverage is 51.7 days (3923bcf/75.8bcf/d. This is about 1.9 days under the 1990-2014 average for that calendar month and 4.1 days beneath 2006-14’s 55.8 day average.

FOLLOW THE LINK BELOW to download this article as a PDF file.

Rollin' and Tumblin' in US Natural Gas (4-20-15)