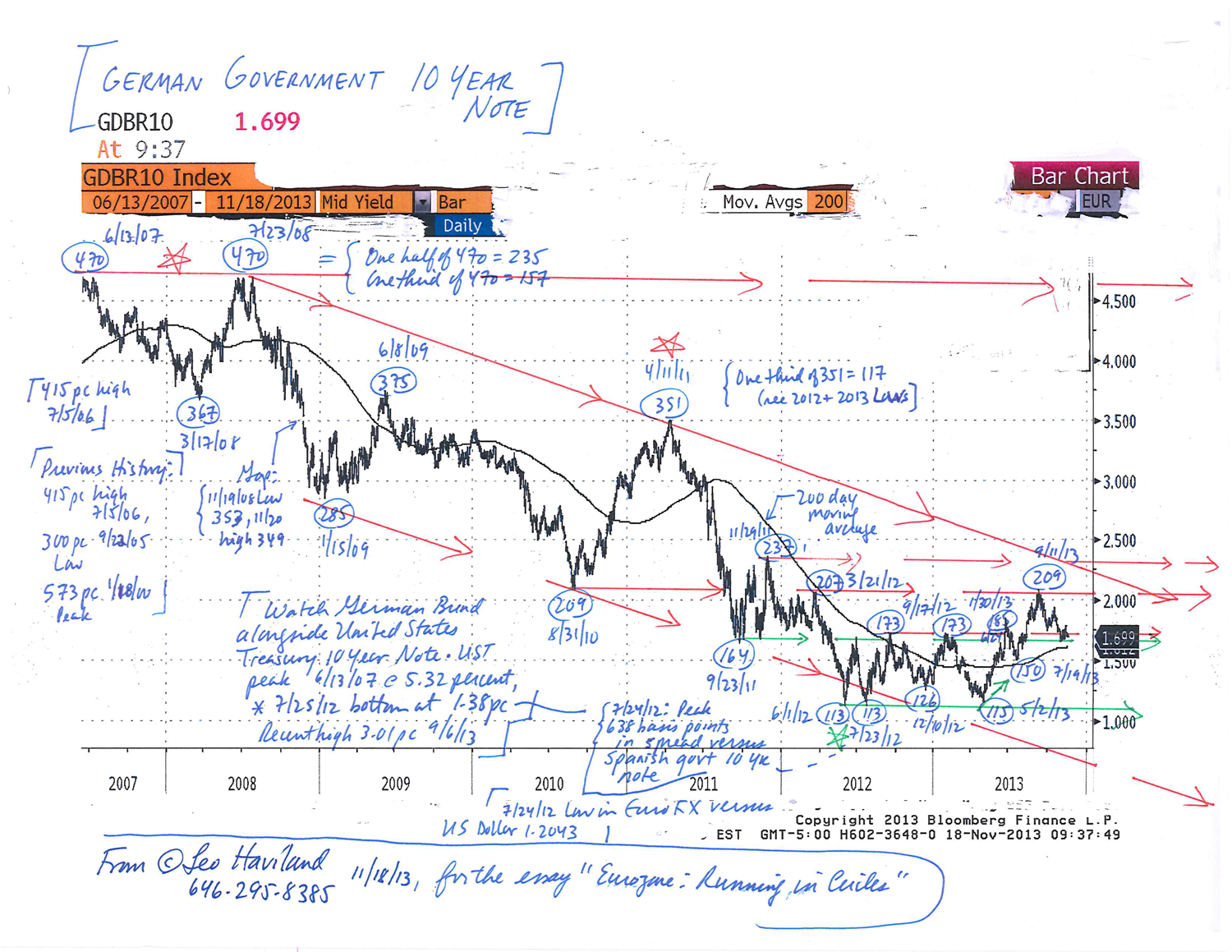

SHAKIN’ ALL OVER: MARKETPLACE CONVERGENCE AND DIVERGENCE © Leo Haviland June 18, 2018

OVERVIEW AND CONCLUSION

Financial wizards not only offer competing opinions regarding past, current, and future trends for stock, interest rate, currency, and commodity marketplaces. Their rhetoric displays diverse viewpoints regarding alleged relationships within and between those categories. For example, within the global stock constellation, various apostles elect to compare the travels of the S+P 500 with those of the Nasdaq Composite or with an emerging marketplace stock benchmark. Alternatively, some visionaries herald their subjective insights and foresights about connections between stocks (such as the S+P 500) and interest rates (such as the United States 10 year government note), perhaps also including the US dollar and the commodities galaxy in their investigations.

Luminaries tell stories offering their cultural perspective regarding apparent convergence and divergence (lead/lag) relationships within and between marketplace domains. Viewpoints regarding convergence and divergence encompass not only price direction (trend), but also the timing (start and end date; duration) of a given move as well as the distance it travelled. In any case, these links (associations; patterns) can alter, sometimes substantially and occasionally permanently. Marketplace history, including that related to convergence and divergence, is not marketplace destiny, whether entirely or even partly.

****

History reveals that the S+P 500 and emerging marketplace stocks “in general” (MSCI Emerging Stock Markets Index, from Morgan Stanley; “MXEF”) often have had very important trend changes in the same direction “around” the same time.

After establishing important bottoms together in first quarter 2016, the key American stock indices and those of other important advanced nations and the “overall” emerging stock marketplace traded closely together from the directional and marketplace timing perspective. Though the bull moves since first quarter 2016 in these assorted domains did not all voyage the same distance, all were very substantial. Their rallies since around the time of the November 2016 United States Presidential election were impressive. Both emerging marketplace equities and the S+P 500 established important peaks in first quarter 2018 (MXEF 1279 on 1/29/18; S+P 500 2873 on 1/26/18).

Yet whereas since its first quarter 2018 summit prices for the emerging stock marketplace arena have eroded significantly and currently rest at their calendar 2018 lows, the S+P 500 has retraced much of its dive and now (6/15/18 close 2780; stock price data in this essay is through 6/15/18) stands only slightly over three percent from its 1Q18 top. This divergence, though not massive, is noteworthy. A similar but more extreme divergence between these stock benchmarks existed from spring 2011 (and note particularly since around second half 2014) through about May 2015. The S+P 500 kept going up and achieved new highs over its spring 2011 one, but the MXEF failed to do so.

After spring 2015, convergence developed, with a bear trend in the S+P 500 accompanying the existing downhill one in the emerging marketplace stock group. An important factor assisting this was the decisive climb in the broad real trade-weighted United States dollar (“TWD”) above its critical resistance around 96.6. A similar convergence is likely to occur in the present MXEF and S+P 500 marketplace relationship, with the significant divergence disappearing and both equity realms falling “together”.

US corporate earnings indeed have been quite strong, with share buybacks and mergers and acquisitions robust. Nevertheless, one bearish factor for stocks in the current landscape is the broad real trade-weighted dollar’s recent advance over the 96.2/96.6 barrier (compare 2015); also recall the TWD rally beginning in spring 2008 during the 2007-09 global economic disaster). The ascending US yield trend (which began in July 2016, accelerating in 1Q18) has encouraged the TWD’s modest rally in the past few months. Trade war talk and potential tariffs probably have assisted the TWD’s appreciation. The US is a net importer nation; some exporters (which include many developing nations) may depreciate their currency to maintain market share within the US.

Another bearish sign for both advanced nation and emerging marketplace stocks is the persistent climb in US Treasury yields. Rising global yields alongside a strengthening dollar is especially painful to emerging marketplace countries and thus their stock marketplaces. Many developing nations, including their corporations, have dollar-denominated debt. And underscore in this context another point: for America over the past century, sustained rising yields generally have led to American stock marketplace declines. Given the Federal Reserve Board’s ongoing tightening policy (and its normalizing balance sheet, as well as probable willingness to allow some overshooting of its two percent inflation target), growing substantial US federal deficits (aided by tax “reform” legislation enacted in December 2017), substantial US household credit demand, a low unemployment rate, and other factors, US government yields probably will tend to keep rising over the long run. The growing mountain of US public debt, including as a percentage of GDP, also tends to push up interest rates.

A confirming sign for equity feebleness in both the S+P 500 and the MXEF likely will be weakness in commodities prices. Commodities often have peaked (bottomed) around the same time as a crucial top (bottom) in important advanced nation or emerging marketplace stocks. However, there have sometimes been lags. Recall that in during the worldwide financial crisis following the glorious Goldilocks Era, commodities “in general” peaked after the S+P 500 and emerging marketplace stocks. The broad Goldman Sachs Commodity Index (“GSCI”) has declined since 5/22/18’s 498 high.

FOLLOW THE LINK BELOW to download this article as a PDF file.

Shakin' All Over- Marketplace Convergence and Divergence (6-18-18)