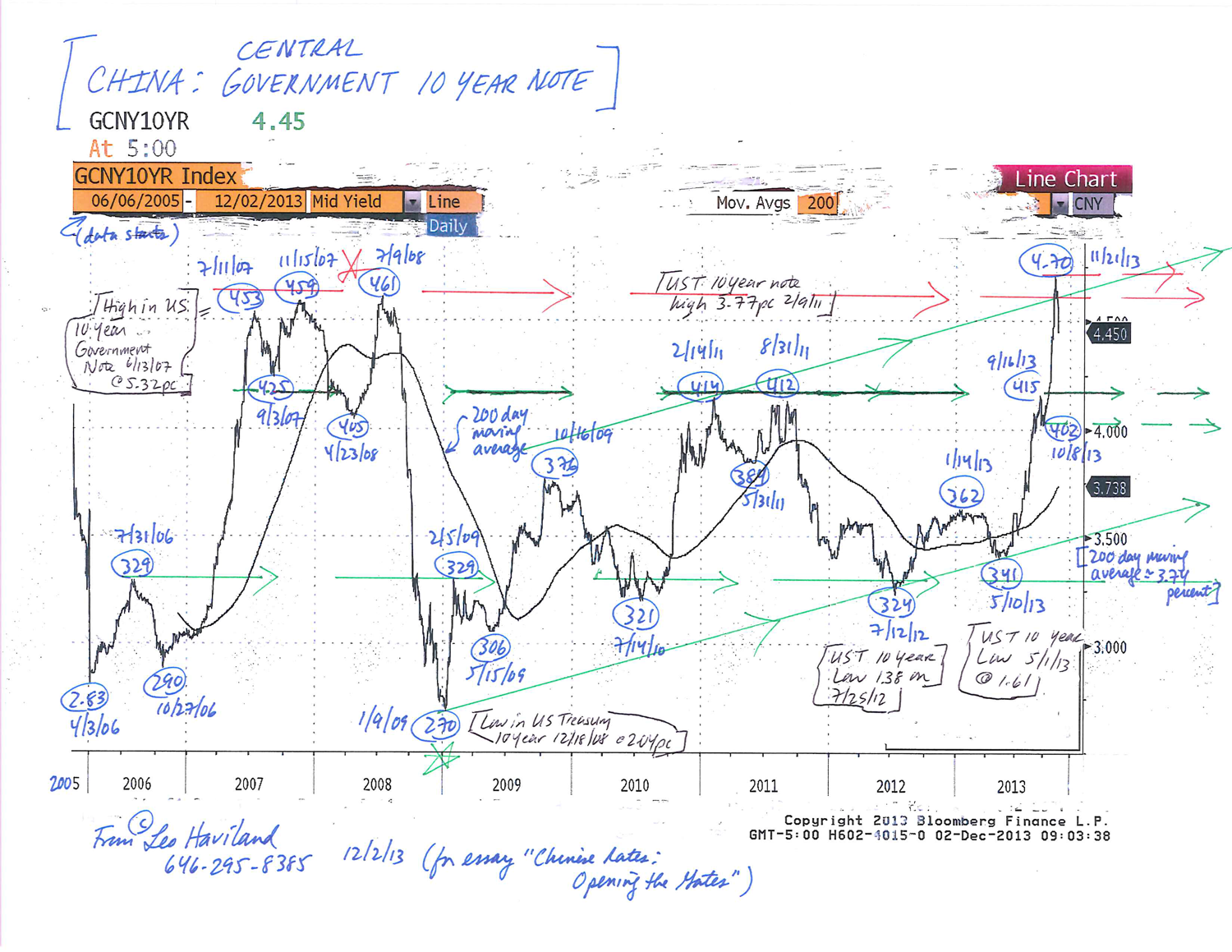

ADVENTURES IN WONDERLAND: COMMODITY CURRENCIES © Leo Haviland September 26, 2016

“For, you see, so many out-of-the way things had happened lately, that Alice had begun to think that very few things indeed were really impossible.” Lewis Carroll, “Alice’s Adventures in Wonderland” (Chapter I)

****

OVERVIEW AND CONCLUSION

Concentrating on and comparing exchange rates of “commodity currencies” offers insight into assorted interrelated marketplace relationships. Since the shocking eruption and terrifying acceleration of the global economic crisis in late 2007/2008, the major price trends for eight “commodity currencies” roughly (and of course not precisely) have ventured forward in similar fashion on a broad real effective exchange rate (“EER”) basis. Over that time, this basket of assorted commodity currencies generally has intertwined in various ways with very significant trends in the broad real trade-weighted United States dollar (“TWD”), emerging marketplace stocks in general, and broad commodity indices such as the S&P Goldman Sachs Commodity Index (“GSCI”).

The substantial rally in the broad real trade-weighted United States dollar (“TWD”) that embarked in mid-2011 played a key part in encouraging (confirming) and accelerating bear movements in emerging marketplace stocks and commodities “in general”. The S+P 500’s monumental rally over its spring 2011 interim high diverged for about four years from the trends in emerging equity realms and commodities. However, the TWD’s late 2015 ascent above its March 2009 peak was a crucial event. This dollar climb helped propel the S+P 500 downhill following 5/20/15’s 2135 pinnacle in conjunction with the emerging stock marketplace and commodity trends.

In January/February2016, these linked price patterns reversed. The TWD has depreciated modestly and stocks (emerging marketplaces as well as those of America and other advanced nations) rallied. Commodities (particularly oil) jumped. The benchmark United States Treasury 10 year note yield initially ascended from its 1Q16 low. This relatively unified reversal across marketplace sectors paralleled the entwined moves since mid-to-late 2015. These current marketplace interrelationships (“roughly trading together”) probably will persist for the near term, regardless of whether the pattern of mid-2015 to first quarter 2016 resumes or that since mid-first quarter 2016 continues. Marketplace history of course need not entirely or even substantially repeat itself.

****

Commodity currencies, associated with countries with large amounts of commodity exports, are not confined to developing/emerging nations. Because commodity exports are important to the economies of advanced countries such as Australia, Canada, and Norway, the currencies of these lands likewise can be labeled as commodity currencies.

The bearish currency paths (effective exchange rate basis) of key emerging and advanced nation commodity exporters up to first quarter 2016 resembled the similar trends among them during the 2007-09 worldwide economic disaster era. However, these commodity currencies depreciated notably more in that recent dive than during 2007-09’s extraordinary turmoil. In addition, the lows attained by most of them decisively pierced the floors achieved about seven years previously. Moreover, the TWD rallied more sharply in its bull leap to its January 2016 elevation than it did during the past crisis.

The feebleness up to the 1Q16 lows for the commodity currency group, as it involved both advanced and emerging marketplace domains (as it did in 2007-09), reflected an ongoing global (not merely emerging marketplace) crisis. Substantial debt and leverage troubles still confront today’s intertwined worldwide economy. The bear trip of many commodity currencies into early first quarter 2016, especially as it occurred alongside big bear moves in emerging marketplace stocks (and in the S+P 500 and other advanced stock battlefields) and despite long-running extremely lax monetary policies, underlined the fragility of the relatively feeble global GDP recovery.

Therefore key central bank wizards, concerned about slowing real GDP and terrified by “too low” inflation (or deflation) risks, have fought bravely to stop the TWD from appreciating beyond its January 2016 top and struggled nobly to encourage rallies in the S+P 500 and related stock marketplaces. Yield repression (very low and even negative interest rates) promotes eager hunts for yields (return) elsewhere. Indeed, rallies in the S+P 500 (and real estate) may help inflation expectations (and inflation signposts monitored by central banks such as consumer prices) to crawl upward. Given their desperate quest to achieve inflation goals, central banks probably approve of at least modest increases in commodity prices as well as appreciation by commodity currencies in general.

****

Noteworthy rallies in these commodity (exporter) currencies from their recent depths tend to confirm (inspire) climbs in commodities in general and emerging (and advanced) nation stock marketplaces. Renewed deterioration of the effective exchange rates of the commodity currency fraternity “in general” likely will coincide with renewed firming of the broad real trade-weighted US dollar. Such depreciation in the commodity currency camp probably will signal worsening of the still-dangerous global economic situation and warn that another round of declines in global stock marketplaces looms on the horizon.

****

“He was an honest Man, and a good Sailor, but a little too positive in his own Opinions, which was the Cause of his Destruction, as it hath been of many others.” “Gulliver’s Travels”, by Jonathan Swift (Part IV, “A Voyage to the Country of the Houyhnhnms”, chapter 1)

****

Looking forward, numerous entangled and competing economic and political variables generate a substantial challenge for explaining and predicting the interconnected financial marketplaces in general, including the commodity currency landscape. The commodity currency group as a whole (“CC”) has appreciated roughly twelve percent from its late calendar 2015/first quarter 2016 depth. What does a review of the adventures in commodity currencies since the assorted late 2015/1Q16 bottoms in the context of other marketplace benchmarks portend? Commodity currencies in general probably are establishing a sideways range. The overall camp of EERs (apart from what may happen to individual ones) will not rally much (if at all) above recent highs. The CC camp eventually likely will renew its overall depreciation, with the various EERs heading toward their noteworthy lows attained several months ago.

Although the CC rally since its 1Q16 bottom retraces some of its prior collapse, the TWD itself has dropped only modestly from its peak and thus remains quite strong. Moreover, note the fall in the broad GSCI (and the petroleum complex) since early June 2016. A still-robust TWD not only underlines potential for renewed weakness in the CC complex, but also confirms commodity feebleness and warns of risks to the recent bull move in emerging marketplace stocks (and even to the astounding S+P 500). China is a key commodity importer. As China’s EER continues to ebb (while Japan’s has strengthened), the ability of the CC clan to produce only a moderate overall percentage rally in their collective EER to date hints that world economic growth remains sluggish. Emerging marketplace stocks in general, despite their rally since 1Q16, remain substantially beneath their September 2014 summit.

Although leading global central banks devotedly retain highly accommodative policies such as yield repression and money printing, the inability of US Treasury 10 year note yield to rise much above its 7/6/16 low at 1.32 percent tends to confirm this picture of unimpressive (and even slowing) global expansion. Optimists underscore the S+P 500’s rally to a new peak on 8/15/16 at 2194 from its 1Q16 trough. Yet that new record elevation merely neighbors May 2015’s plateau, exceeding it by just 2.8 percent.

****

There is significant marketplace and political talk of trade wars, growing protectionism, and anti-globalization. Much of this wordplay links to populist challenges to the so-called establishment (elites). But even some establishment politicians have become less enamored of free trade. Fears of trade conflicts and protectionist barriers weigh on the CC domain as a whole.

For commodity currencies, much depends on Federal Reserve policy. At present, although the Fed did not boost rates in September, it currently seems fairly likely to do so in December 2016 (assuming no dramatic drop in stocks occurs before then). Especially as the European Central Bank, Bank of England, and Bank of Japan remain married to their highly accommodative schemes, this Fed action will help to rally the TWD and thus tend to weaken the CC armada. Nevertheless, the Fed and other central banks probably will fight to keep the dollar from surpassing its 1Q16 summit; doing so helps to protect stock (and real estate) prices and thus to reduce populist political advances.

The result of the US Presidential election on November 8 naturally remains uncertain. Unlike the EERs of the other seven commodity currencies, the Mexico EER has slumped beneath its first quarter 2016 low. Mexico faces severe domestic political challenges, and ongoing low oil prices wound its economy. However, the increasing potential for a Trump victory and resulting trade conflicts and immigration disputes also have helped to push Mexico’s EER downhill. The Mexican peso crisis of the early 1990s should not be forgotten.

Significant ongoing American political divisions risk further weakness in the US dollar, regardless of who wins the exciting Presidential sweepstakes. The US has a long run budget challenge regardless of who emerges victorious. Though the TWD issue is complex, a Trump victory likely is more bearish for the TWD than a Clinton one. Comments from overseas (and numerous domestic) leaders suggest lack of confidence in Trump’s abilities and policies, which arguably would be reflected in reduced acquisition (or net selling) of dollar-denominated assets such as US government securities (and corporate debt) and American stocks. Trump’s budget proposals, if enacted, will likely expand the deficit considerably and thus probably would encourage interest rate rises. A Trump triumph likely would be bearish for the US dollar in general, even if the dollar rallied against the Mexican peso on a cross rate basis. However, though numerous respected forecasters predict a close outcome, Clinton probably will defeat Trump. In any case, all else equal, a Democratic victory increases the odds of a Fed rate hike in the near term.

FOLLOW THE LINK BELOW to download this article as a PDF file.

Adventures in Wonderland- Commodity Currencies (9-26-16)