GLOBAL ECONOMICS AND POLITICS

Leo Haviland provides clients with original, provocative, cutting-edge fundamental supply/demand and technical research on major financial marketplaces and trends. He also offers independent consulting and risk management advice.

Haviland’s expertise is macro. He focuses on the intertwining of equity, debt, currency, and commodity arenas, including the political players, regulatory approaches, social factors, and rhetoric that affect them. In a changing and dynamic global economy, Haviland’s mission remains constant – to give timely, value-added marketplace insights and foresights.

Leo Haviland has three decades of experience in the Wall Street trading environment. He has worked for Goldman Sachs, Sempra Energy Trading, and other institutions. In his research and sales career in stock, interest rate, foreign exchange, and commodity battlefields, he has dealt with numerous and diverse financial institutions and individuals. Haviland is a graduate of the University of Chicago (Phi Beta Kappa) and the Cornell Law School.

Subscribe to Leo Haviland’s BLOG to receive updates and new marketplace essays.

Nevertheless, although the Euro Area “in general” is not entirely out of gas and running on empty, it is running in place. Its economic performance for the next few years probably will be sluggish. There will be little or no economic growth, general government debt will remain quite high, and unemployment will stay very lofty.

The Eurozone economy is going nowhere fast on the road to recovery. Of course differences between individual nations exist; Germany is not Greece.

For the stock arena, take the SXXP index of 600 European stocks (though it includes United Kingdom and other non-Euro Area companies) as a benchmark (Bloomberg symbol is SXXP). This vehicle, like America’s S+P 500, has not moved in a sideways pattern, but instead has (despite some sharp twists and turns) flown sky-high since its 3/9/09 major low at 155.4 (S+P 500 major trough 3/6/09 at 667). The bottom line is that the probable path of European equities probably is closely bound with that of American stocks.

With the SXXP now around 325.0, what’s the rundown on some SXXP levels to monitor? Recall 332.9, the 5/19/08 high. The final top in the S+P 500, after its 10/11/07 pinnacle at 1576, also occurred 5/19/08 (at 1440). If prices fall from current levels, note that twice the 3/9/09 bottom is 310.8; keep an eye on 2/18/11’s 292.2 if prices stumble further. Unlike the S+P 500, the SXXP has not escaped above its 2007 peaks. Are prices for European equities circling back to their former record heights? In any event, if European stock prices venture even higher from current levels, watch 10/11/07’s summit at 391.3 and the major pinnacle of 401.0 on 7/13/07.

FOLLOW THE LINK BELOW to download this market essay as a PDF file.

Eurozone- Running in Circles (11-18-13)

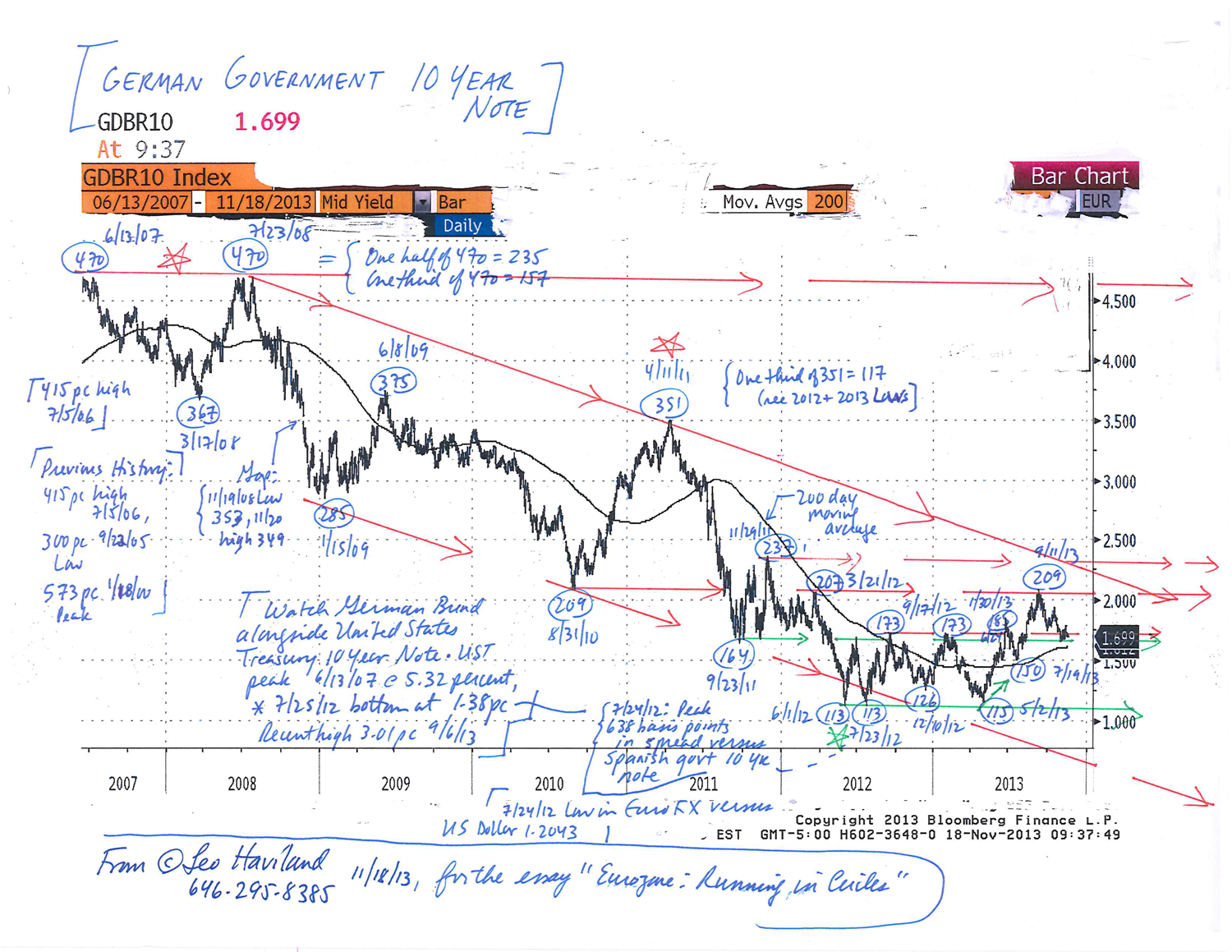

Chart- German Govt 10 Year Note (for essay, Eurozone- Running in Circles) (11-18-13)

The decline in the Euro FX does more than reflect Europe’s sovereign debt and banking crisis. Europe does not stand or act alone. Euro currency weakness underlines the continuing epic worldwide economic disaster that emerged in 2007. The sustained slump in the Euro FX since spring 2011 warns that the worldwide economic recovery that began around early 2009 is slowing. Some headway has been made in containing Eurozone (and other European) problems, but that progress has been insufficient and it probably will remain so for at least several more months. The Euro FX will depreciate further from current levels.

First, despite the major sovereign debt and banking problems, the Eurozone’s political and economic leadership has the political desire and (ultimately) sufficient economic power to preserve the Eurozone. This means keeping even members such as Greece within it. The problems of the so-called peripheral nations in key respects have become those of the entire fraternity. The Eurozone may rely on outside economic help from the International Monetary Fund or other countries to help pay for the repairs. However, the region as a whole will, “if push comes to shove”, resolve the thorny difficulties itself. And even if Greece did exit the Eurozone, remaining Eurozone members probably would band together to keep the Eurozone intact.

For some time, the so-called fixes may involve pushing the problem (dangers) off to a more distant future. The buying-time strategies (hoping that economic recovery eventually will enable a genuine escape) of course will have some costs. For example, picture inflation risks, slower growth, and some suffering by creditors.

The substantial role of the Euro FX in official reserves underlines the importance of the Eurozone and its Euro FX in the world economic order. Most of the world surely does not want the Euro FX to disappear entirely, or to suffer a massive depreciation (as opposed to a further small or even a modest depreciation). Thus at some point (“if really necessary”), the world outside of Europe would ultimately bail out Europe.

Consequently the declines in the Euro FX over the past several months confirm worldwide economic sluggishness (and slumps in stock marketplaces and commodities). So further falls in the Euro FX may reflect- or help lead to- even more declines in equity and commodity playgrounds. That additional Euro FX debasement may even reflect or accelerate an economic downturn (not just stagnation) in some regions, and not just European territories. Thus Euro FX currency depreciation alone will not solve the Eurozone’s (or overall European) problems.

FOLLOW THE LINK BELOW to download this market essay as a PDF file.

Eurozone- Breaking Up Is Hard To Do (1-3-12)