AMERICAN HOUSING: A MARKETPLACE WEATHERVANE © Leo Haviland December 4, 2018

“What You Own”, a song from the musical “Rent” (by Jonathan Larson), declares: “You’re living in America at the end of the millennium- you’re living in America, where it’s like the twilight zone.”

****

OVERVIEW AND CONCLUSION

American home prices have enjoyed a joyous climb since their dismal lows following the global economic disaster of 2007-09. However, United States home prices “in general” (“overall”) now probably are establishing an important peak. At least a modest reversal of the magnificent long-run bullish United States home price trend probably is near.

What is a high (too high), low (too low), expensive, cheap, average, good, bad, neutral, normal, typical, reasonable, commonsense, appropriate, fair value, overvalued, undervalued, natural, equilibrium, rational, irrational, or bubble level for prices or any other marketplace variable is a matter of opinion. Subjective perspectives differ. In any case, current US home price levels nevertheless appear quite high, particularly in comparison to the lofty heights of the amazing Goldilocks Era. As current American home price levels (even if only in nominal terms) hover around or float significantly above those of the Goldilocks Era, this hints that such prices probably are vulnerable to a noteworthy bearish move. Moreover, measures of global home prices and US commercial real estate also have surpassed their highs from about a decade ago and thus arguably likewise may suffer declines.

Many United States housing indicators in general currently appear fairly strong, particularly in relation to their weakness during or in the aftermath of the global economic crisis. Nevertheless, assorted American housing variables as well as other phenomena related to actual home price levels probably warn of upcoming declines in American home (and arguably other real estate) prices. A couple of US home price surveys have reported price declines for very recent months. US housing affordability has declined. New single-family home sales display signs of weakness, as do new privately-owned housing starts. American government interest rate yields, as well as US mortgage rates, have edged up. The Federal Reserve Board as of now likely will continue to tighten and raise rates for a while longer. Overall household debt, though not yet burdensome (at least for many), now exceeds the pinnacle reached ten years ago in 3Q08. The economic stimulus from America’s December 2017 tax “reform” probably is fading. US consumer confidence dipped in November 2018.

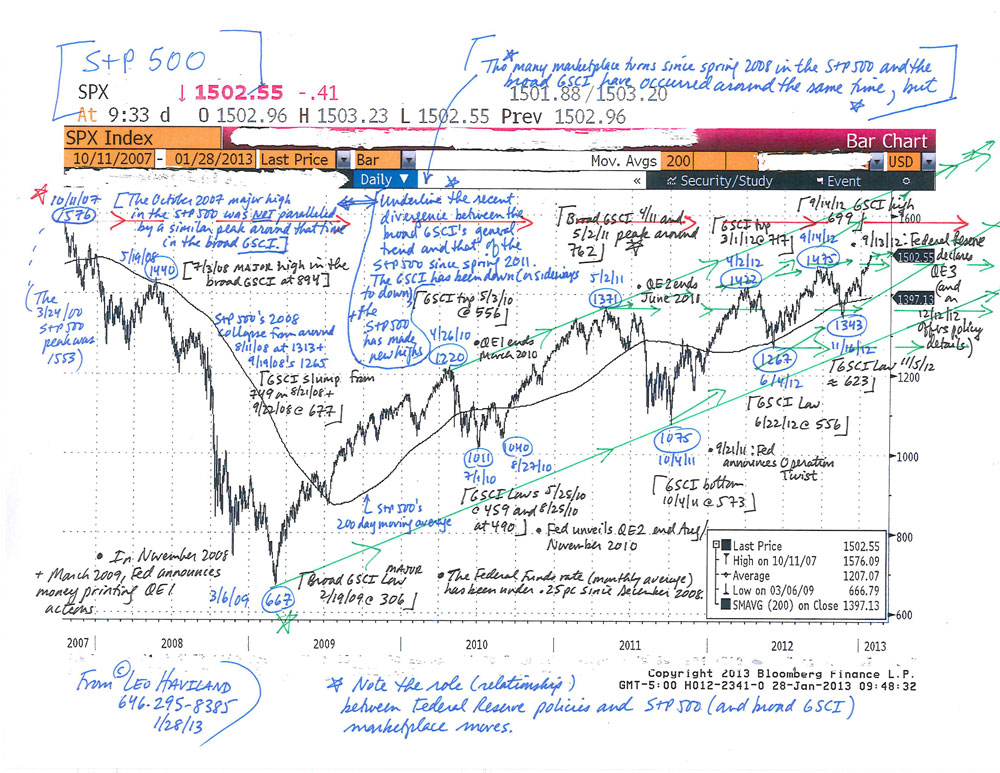

Marketplace history of course does not necessarily repeat itself, either entirely or even partly. Convergence and divergence (lead/lag) relationships between marketplace trends and other variables can shift or transform, sometimes dramatically. Price and time trends for the American stock marketplace and US housing prices do not move precisely together. However, the international 2007-09 crisis experience (which in part strongly linked to US real estate issues) indicates that prices for US stocks and housing probably will peak around the same time, or at least “more or less together” (a lag of several months between the stock high and the home price pinnacle). The S+P 500 probably established a major high in autumn 2018 (9/21/18 at 2941, 10/3/18 at 2940; the broad S&P Goldman Sachs Commodity Index peaked 10/3/18 at 504). That autumn equity summit in the S+P 500 bordered 1/26/18’s interim top at 2873. Ongoing weakness in US (and international) stock marketplaces will help to undermine American home prices.

FOLLOW THE LINK BELOW to download this article as a PDF file.

American Housing- a Marketplace Weathervane (12-4-18)