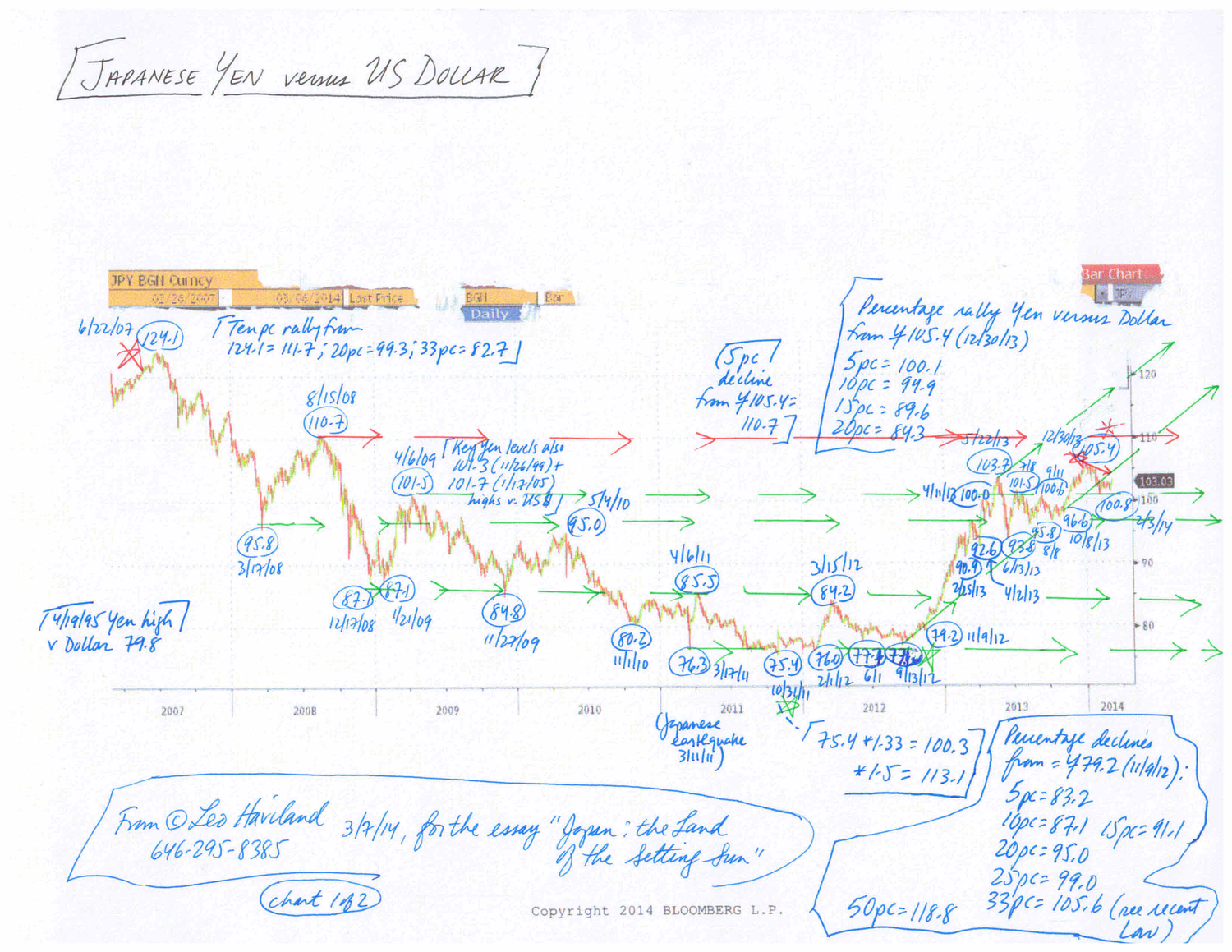

TICKET TO RIDE: US CORPORATE PROFITS AND S+P 500 TRENDS (c) Leo Haviland, May 17, 2017

In “Ticket to Ride”, The Beatles sing:

I don’t know why she’s riding so high

She ought to think twice

She ought to do right by me

Before she gets to saying goodbye”.

****

CONCLUSION AND OVERVIEW

In offering enthusiastic audiences explanations of past, current, and future United States stock marketplace levels and travels, diverse marketplace preachers tell competing tales. Their arguments and conclusions reflect their different marketplace perspectives and methods, including the particular variables they select and arrange. For a majority of devoted visionaries, American corporate profitability is a very important factor.

****

After-tax US corporate profits soared after reaching a trough in fourth quarter 2015, not long before the S+P 500’s major bottom in first quarter 2016. The noteworthy profit climb since 4Q15 surely encouraged the S+P 500 to jump from its 1Q16 trough.

Yet Trump’s remarkable triumph in November 2016’s Presidential election created (or at least magnified) faith that United States after-tax corporate profits would increase significantly in calendar 2017 and 2018. The S+P 500 galloped 15.2 percent higher from 11/4/16’s 2084 low to 3/1/17’s 2401 elevation. Thus hopes for greater profits probably greatly assisted the S+P 500’s sharp rally.

What is a key tenet (especially in the post-election period) in the gospel promoting a viewpoint of growing American corporate profitability and an entangled bull stock climb? Much centers on hopes that the Republican-controlled Congress will enact noteworthy corporate tax cuts. Related optimism for marketplace earnings (and stock) bulls includes possibilities for repatriation of corporate cash hoards, dramatic boosts in domestic infrastructure spending, and reduced regulatory burdens.

****

However, current sharp divides on the American political scene (including within the Republican congregation) and widespread lack of confidence in (and hostility toward) the President will make it very difficult for a notable change in the corporate (and individual) tax code to become law. Passage of legislation encouraging earnings repatriation is not assured. Moreover, neither is a monumental infrastructure spending scheme.

In addition, despite the fierce climbs in recent calendar quarters, profit highs for recent full calendar years do not manifest a clear trend toward moving to new heights. Full calendar year profits over the past few years have been about flat.

Disappointment relative to widely-forecast profitability gains may inspire S+P 500 price retreats. In any case, history reveals that several noteworthy bear moves in the S+P 500 have intertwined with noteworthy profitability slumps.

****

What is too high (too low), high (low), overvalued (undervalued), or reasonable/rational/average/normal (unreasonable, irrational, atypical/abnormal) for stock prices or other economic indicators is a matter of opinion. However, and even though stock valuations can appear very elevated relative for an extended period of time, some marketplace gurus nowadays proclaim that some measures show US stock valuations are on the lofty side.

Also, elevated share buyback levels also have helped to propel US equities higher. There are hints this pattern will not persist.

Current low US stock marketplace volatility, high American consumer confidence, and evidence that financial stress remains below average have reflected (and encouraged) the majestic bull climb in the S+P 500. Observers nevertheless should watch for changes in such measures.

A warning light for S+P 500 bulls is the failure the S+P 500 to motor much above the early March 2017 high. The subsequent record high is 5/16/17’s 2406. If the S+P 500 continues to find ventures much beyond that March 2017 elevation challenging, this arguably will signal that current optimism regarding future corporate profit gains may be ebbing, that the S+P 500 bull trend is tiring, or both.

****

So the failure of America to enact important corporate tax “reform” (tax cuts) or embark on a glorious infrastructure spending voyage may not greatly diminish future earnings expectations (or even actual levels) or significantly wound the S+P 500. But they might.

****

In addition, challenges to the bullish trend in US equities may come from the long run upward trend of US government interest rates (note the Fed’s tightening plan). Or, concern about US federal budget deficits (or debt problems elsewhere in the world) may march into view. Hopes for higher (or at least not falling) energy prices likely underpin hopes for higher corporate earnings (and profits) in that key financial sector. But commodities “in general” (and petroleum in particular) have fallen from their 1Q17 highs. Anticipated oil output levels from OPEC and its non-OPEC comrades probably will not significantly reduce still-high OECD industry inventories for at least the next several months. The broad real trade-weighted US dollar established highs in December 2016/January 2017, though it has slipped only modestly since then. Contrary to what many believe, increasing US dollar depreciation may help lead to or confirm weakness in the US stock marketplace.

****

FOLLOW THE LINK BELOW to download this article as a PDF file.

Ticket to Ride- US Corporate Profits and S+P 500 Trends (5-17-17)